The changes to the meals and entertainment (“M&E”) and employee fringe benefits has been one of the most confusing and misunderstood areas under the new Tax Cuts and Jobs Act (“TCJA”). As more information becomes available about the TCJA, there appears to be some consensus as to what M&E and employee fringe benefit expenses will qualify for a deduction either in whole or in part and what, if any, expenses are non-deductible.

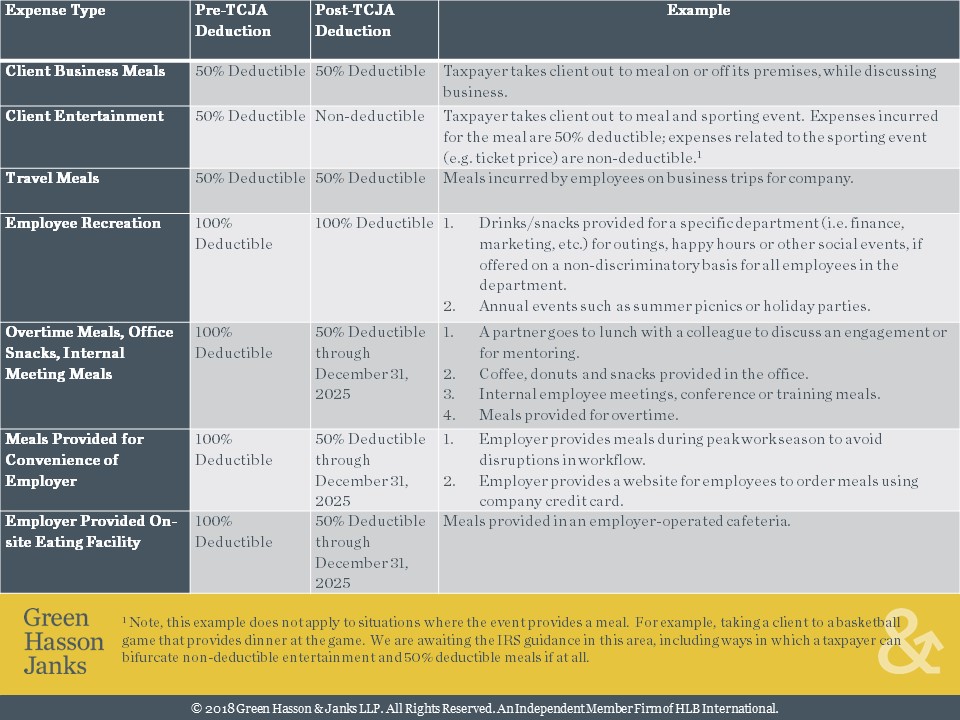

Under the pre-TCJA law, a 50-percent deduction for ordinary and necessary expenses for entertainment, amusement, or recreation was allowed to the extent the expenses were directly related to or associated with the active conduct of the taxpayer’s trade or business. In addition, some meals such as meals provided in an employer-operated eating facility or other de minimis meals were 100-percent deductible for tax purposes.

The TCJA has changed the tax treatment of M&E expenses and employee fringe benefits. One significant change is the complete elimination of the deduction for business entertainment expenses as well as reductions in the amount that can be deductible for employer provided meals. Effective Jan. 1, 2018 the TCJA modifies Section 274 by eliminating the deduction for business entertainment expenses. Expenses related to client or employee business meals and beverages, however, remain 50-percent deductible. Effective for the period Jan. 1, 2018 through Dec. 31, 2025, employer provided meals and other de minimis meals remains deductible, but the deduction amount has been reduced from 100 percent to 50 percent. After Dec. 31, 2025, employer provided meals and other de minimis meals are 100-percent nondeductible.

Given the changes under the TCJA to meals and entertainment and employee fringe benefits, it will become important that taxpayers maintain separate accounting and documentation for the cost of business meals and entertainment so deductible meals and nondeductible entertainment expenses can be tracked accurately. Taxpayers must meet substantiation requirements to qualify for any meal expenditure deductions. This includes substantiating the amount, time and place of the meal, business purpose and other requirements as necessary. Upon an audit by the Internal Revenue Service (“IRS”) and/or state taxing authorities, this will likely be one area that is heavily scrutinized and therefore proper documentation and accounting will be important.

Below is a high-level overview of the changes made to the M&E and employee fringe benefits deduction, a summary of deductibility percentages and some practical examples of typical M&E and employee fringe benefits that many taxpayers incur as part of their active trade or business.

As more information becomes available, particularly guidance provided by the IRS, GHJ will provide further Tax Alerts accordingly. For more information on how these changes may impact you, contact us a GHJ Tax Advisor at 310.873.1600.