For fiscal year 2018, approximately 5.1 million S corporation tax returns were filed, which outnumber partnerships (approximately 4.2 million tax returns) and C corporations (approximately 2.1 million tax returns), according to the Internal Revenue Service (“IRS”). It is pretty clear that an S corporation is a popular choice for many business enterprises.

As mergers and acquisitions (“M&A”) activity has been strong in the past few years, we have seen a number of M&A transactions involving S corporations. For income tax purposes, M&A transactions involving an S corporation bring certain unique opportunities and obstacles. This blog will discuss some of those opportunities as well as obstacles. In particular, this article will discuss a situation when certain shareholders of an S corporation prefer to sell all of their interests while the remaining shareholders prefer to rollover some of their interests with the buyer.

What is an S corporation?

An S corporation is generally any corporation that:

- Makes an election to be treated as an S corporation by filing IRS Form 2553

- Meets all of the requirements to be an S corporation since election

While this blog is not intended to provide a detailed analysis of the requirements to be a valid S corporation, an S corporation may not:

- Have more than 100 shareholders

- Have a shareholder who is not an individual

- Have a nonresident alien as a shareholder

- Have more than one class of stock

There are various exceptions and other rules within these requirements, so companies should consult their business advisor for clarification.

The Treasury regulation defines one-class stock as outstanding stock having identical rights to distribution and liquidation proceeds. As such, S corporations generally must allocate profit, loss and distributions pro rata among their shareholders based on ownership percentages.

Advantages of S corporations in M&A

When the shareholder(s) of an S corporation decide to sell the S corporation, they typically want long-term capital gain tax treatment in order to take advantage of the preferential tax rates. On the other hand, most buyers typically want to achieve a step-up in the tax basis of the S corporation’s assets in order to depreciate and/or amortize such basis after the transaction. In many cases, the buyer’s objective and the seller’s objective create a direct conflict.

However, with proper structuring, S corporations can generally accommodate both the buyer’s and the seller’s objectives without incurring significant incremental tax costs. There are several permutations to achieve the sale of an S corporation’s assets for tax purposes:

- Sale of assets

- Sale of stock with a section 338(h)(10) or section 336(e) election

- Formation of a new holding company on top of the existing S corporation, followed by the conversion of the existing S corporation into a limited liability company (what is typically referred to as “F Reorg Structure”)

In a sale or deemed sale of an S corporation’s assets, the seller may face ordinary income from certain items such as depreciation recapture, gain in inventory, cash-basis receivables, etc. However, the buyer typically gets a tax benefit for these items. As such, both parties may be willing to work together. Perhaps the buyer covers the seller’s incremental tax costs of buying the S corporation’s assets.

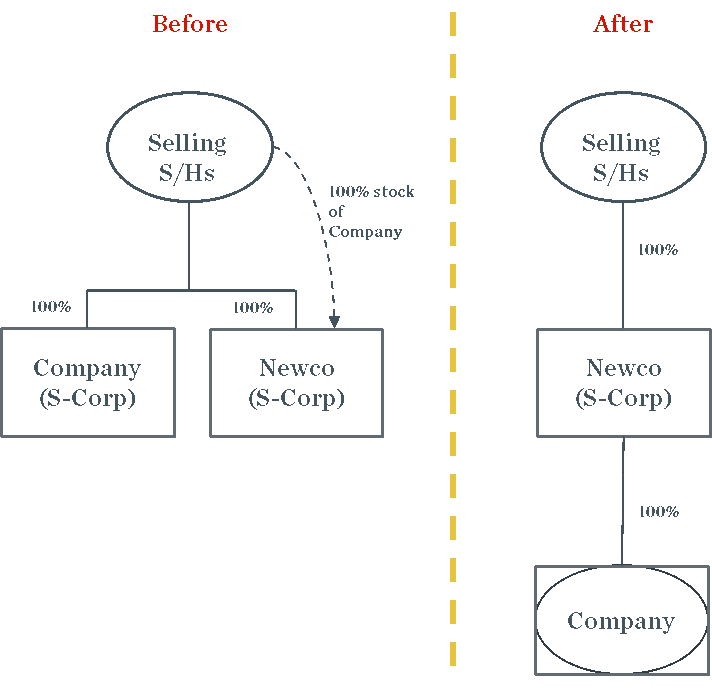

The F Reorg Structure has gained a great deal of popularity due the fact that it generally allows a tax-deferred rollover. The below structure illustrates one of the most common F Reorg Structure scenarios:

Step 1: Restructuring

Prior to the sale, the selling shareholders need to complete a restructuring transaction where a new corporation (“Newco”) is formed and the existing company (“Company”) is contributed. At the same time, an election to treat Newco as an S corporation should be made, and the Company may be converted into a limited liability company. If properly executed, this step should be a reorganization under section 368(a)(1)(F).

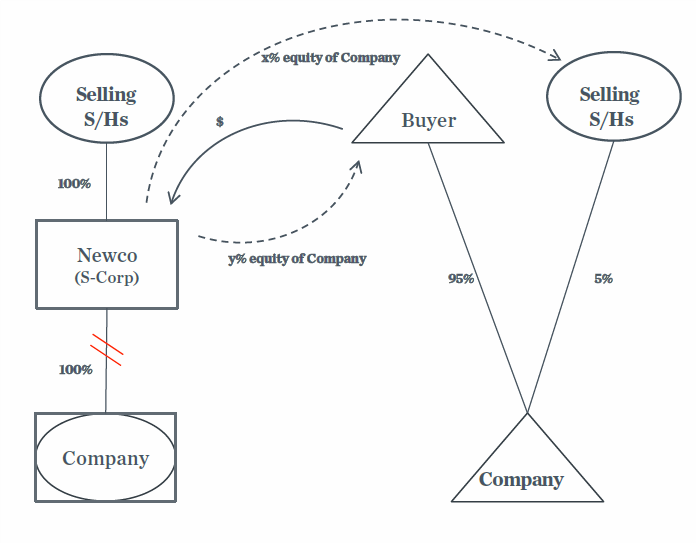

Step 2: Sale

In Step 2, the buyer acquires X percent of the Company in exchange for cash or other consideration. As a result, after the transaction, the buyer and Newco will own collectively 100 percent of the Company, which then should be treated as a partnership for tax purposes. This allows the buyer to get a step-up in the tax basis of the Company’s X percent of assets, and Newco to recognize the gain on X percent of the Company, rather than 100 percent.

By having the F Reorg Structure, the buyer can achieve a step-up in the tax basis in the Company’s assets proportionate to its cash or other consideration, and Newco only recognizes gain on the portion that it sold for such consideration[1].

Obstacles of S corporations in M&A

Despite the fact that S corporations allow various structuring alternatives to allow a tax efficient sale or partial sale, the one-class of stock requirement for S corporations sometimes becomes a roadblock. In the above F Reorg Structure, since Newco recognizes the gain on the sale of X percent of the Company, the gain should be allocated to the selling shareholders based on their respective ownership percentage. This is generally fine as long as every shareholder wants to retain its interests in Newco.

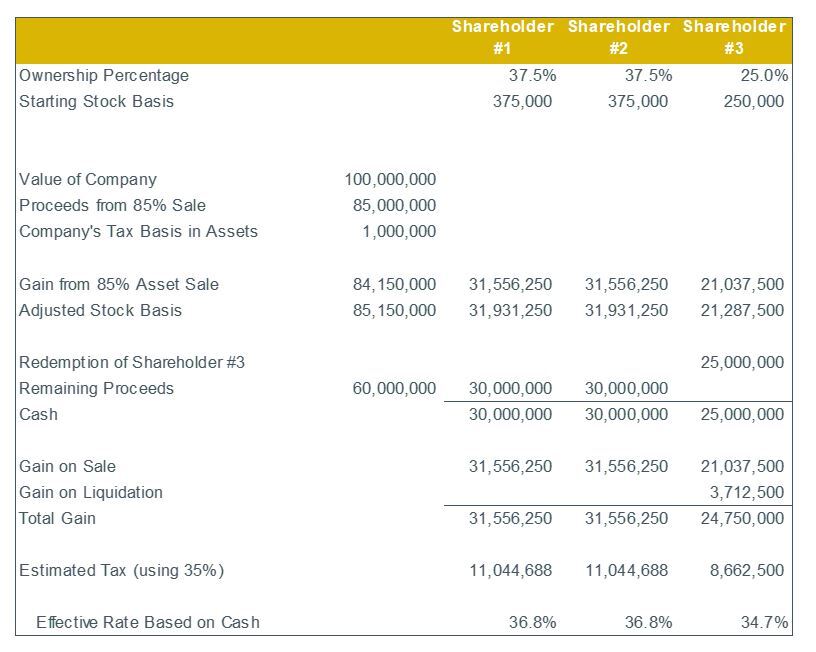

However, if a particular shareholder wants to completely depart from Newco in exchange for cash or other consideration, this creates an issue. While the gain is still recognized based on the current ownership percentages, someone will get disproportionately more cash than the others. The table below illustrates this issue.

[1]While it is not a focus of this article, an S corporation is still a corporation. Thus with the right facts, a reorganization under section 368 may be possible for an M&A transaction involving S corporations. The F Reorg Structure is one such benefit.

Here, Shareholder #1 and #2 want to sell a portion of their interests in the business and retain the remaining portion, whereas Shareholder #3 wants to “cash out” completely. Collectively, these shareholders are selling 85 percent of the company for cash and rolling over 15 percent with the buyer.

Shareholder #1 and #2 each recognizes 37.5 percent of the gain by virtue of their ownership percentages, while receiving only approximately 35.29 percent of proceeds. This means that shareholder #1 and #2 are likely to end up with a higher stock basis in Newco going forward by recognizing more gain than cash being distributed. This may not be the most efficient tax result for Shareholder #1 and #2.

Imperfect Solutions

There are some ways to mitigate this obstacle, but none of them appear to be perfect.

- Redemption: One way to ameliorate this issue is long before the transaction is being contemplated, the company may consider redeeming out those who may depart from the company. The S-corporation rules generally permit a buy-sell and redemption agreement so long as a principal purpose of the agreement is not to avoid the one-class of stock rule and a purchase price is not significantly in excess of or below the fair market value of the stock when such agreement is entered into. The Treasury regulations provide that “…book value or at a price between fair market value and book value are not considered a price that is significantly in excess of or below the fair market value…”

- Partnership: Alternatively, the shareholders may effectuate Step 1 sometime before the sale, and then the Company issues a profits interest to those shareholders who perform services for the Company and are likely to remain with the Company (“Rollover Shareholders”). As such, some or all of future appreciation of the Company after Step 1 belongs to the Rollover Shareholders. The main downside of this solution is that the seller may reduce the issue identified in Step 2 but might not completely eliminate such issue.

- Stock Deal: If a step-up in the basis of the Company’s assets is not important to the buyer or such step-up is immaterial, perhaps the easiest way to effectuate the transaction is a stock sale where each shareholder sells the Company’s stock to the buyer.

The downside of this solution is that if the redemption is so close to the actual transaction, the IRS may collapse the redemption and sale into a single transaction. In addition, it may be hard to predict which shareholder(s) will completely depart from Newco unless there is a pending transaction to sell a portion of the Company. In some cases, the transaction itself may create tension to have someone depart from Newco.

In summary, there does not appear to be a perfect solution if you have an S corporation going through a partial sale in which not all of the shareholders want to retain their interests in the business. Unfortunately, this issue may not surface until there is a deal on the table. To the extent this issue can be anticipated in advance, there may be some planning that can be done to alleviate this issue.

Takeaways

M&A transactions involving S corporations are generally flexible, and there are several planning opportunities to achieve the objectives of the parties involved in the transactions. However, there are still certain obstacles to navigate through.

If you are contemplating a transaction involving an S corporation, please contact the dedicated transaction tax team at GHJ.