Washington Business and Occupation Tax

On March 14, 2019, Washington Governor Jay Inslee signed into legislation Substitute Senate Bill 5581, which made changes to certain economic nexus provisions under the state of Washington Business and Occupation (“B&O”) and sales taxes.

The state of Washington adopted new threshold for B&O and sales tax effective Jan. 1, 2020. A business will have nexus in Washington under its B&O and sales taxes if its “combined gross receipts” from the state are over $100,000 in the current or immediately preceding calendar year. Thresholds will apply to all Washington income, including retailing, wholesaling, service and other activities, and other apportionable activities.

In addition, the business will be subject to B&O tax if it has a physical presence, or is commercially domiciled or organized in the state. The prior B&O nexus thresholds related to property and payroll, as well as the rule creating nexus if 25 percent of property, payroll or sales are in Washington, are eliminated.

Notably, bill E2SHB 2158 becomes effective Jan. 1, 2020 as well and imposes various surcharge rates on certain businesses that report gross receipts under the “Service and Other Activities” classification of the B&O tax. The current rate is 1.5 percent and continues to apply to non-enumerated activities. Businesses that are primarily engaged in 43 listed activities are subject to a 20-percent surcharge for a total rate of 1.8 percent. Additional surcharges are effective Jan. 1, 2020 for certain advanced computing taxpayers and financial institutions.

Update:

On Feb. 10, 2020, Washington Gov. Inslee signed ESSB 6492, repealing the B&O tax surcharges on certain service-based gross receipts and advanced computing businesses enacted through E2SHB 2158, in favor of a simplified system. ESSB 6492 modifies the B&O tax surcharges as follows:

● Repeals the 20-percent surcharge on designated service-based businesses and the surcharges on advanced computing businesses enacted in 2019, effective from Jan. 1, 2020

● Increases the current 1.5-percent service and other activities B&O tax rate on service-based gross receipts to 1.75 percent for all businesses with gross income of one million dollars or more (except hospitals and large advanced computing businesses), effective April 1, 2020

Voluntary disclosure applications (“VDA”) are available for the B&O tax. However, taxpayers are not eligible if they register for the tax before applying for the VDA or have previously been contacted by the state regarding the tax. The above nexus changes are effective this year, but liability may exist for prior years based on previous nexus thresholds.

Update:

The Washington Department of Revenue is temporarily expanding the eligibility criteria for the VDA Program, effective July 15, 2020 through Nov. 30, 2020. Businesses whose most recent enforcement contact was prior to July 1, 2019. Businesses who have not been named as an affiliate of another business through an enforcement contact.

Oregon Commercial Activity Tax

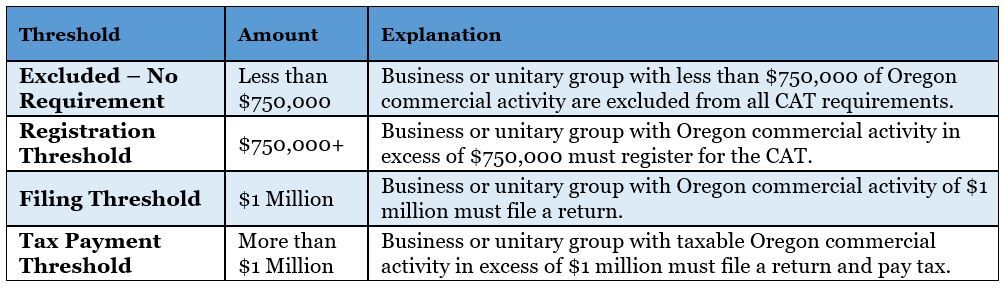

On May 16, 2019, Oregon Governor Kate Brown signed House Bill 3427, legislation that creates Oregon’s first modified gross receipts tax, the Corporate Activity Tax (“CAT”). The Oregon CAT will be imposed on taxable commercial activity in excess of $1 million at the rate of 0.57 percent, plus a flat tax of $250 on the taxpayer’s first $1 million of taxable commercial activity. Taxable commercial activity for Oregon purposes is generally Oregon gross receipts and allows for a subtraction of 35 percent of Oregon costs of goods sold or specified labor costs. Specific types of entities (i.e., government, tax, exempt, etc.) are exempt from the tax, and there are many revenue exclusions from the commercial activity definition (i.e., interest, insurance proceeds, pass-through income, certain taxes, etc.).

Who is subject to CAT?

Any business, or unitary group of businesses, doing business in Oregon may have responsibilities under the CAT. This includes all business entity types, such as C and S corporations, partnerships, sole proprietorships and other entities. Only entities with activity in Oregon are subject to the tax, meaning only lower-tier or operating flow-through entities are taxable.

Filing frequency: For quarterly filers, estimated payments are due April 30, July 31, Oct. 31 and Jan. 31 for the preceding calendar quarter. A taxpayer expecting $5,000 or less of CAT liability for a calendar year does not need to make estimated payments but still must file an annual return on April 15 of the following calendar year. The first annual return is due April 15, 2020. Six-month extensions are available under good-cause requirements for the annual return.

Need more details on the impact to your business? Contact GHJ Tax Advisors for additional information to determine filing requirements in Washington and Oregon.